Declining Energy Quality Could Be a Root Cause of Current Recession

November 30, 2010

An overlooked cause of the economic recession in the U.S. is a decade long decline in the quality of the nation’s energy supply, often measured as the amount of energy we get out for a given energy input, says energy expert Carey King of The University of Texas at Austin.

Many economists have pointed to a bursting real estate bubble as the initial trigger for the current recession, which in turn caused global investments in U.S. real estate to turn sour and drag down the global economy. King suggests the real estate bubble burst because individuals were forced to pay a higher and higher percentage of their income for energy-including electricity, gasoline and heating oil-leaving less money for their home mortgages.

In economic terms, the quality of the nation’s energy supply is referred to as Energy Return on Energy Investment (EROI). For example, if an oil company uses a 10th of a barrel of oil to drill, pump, transport and refine one barrel of oil, the EROI for the refined fuel is 10.

“Many economists don’t think of energy as being a limiting factor to economic growth,” says King, a research associate in the university’s Center for International Energy and Environmental Policy. “They think continual improvements in technology and efficiency have completely decoupled the two factors. My research is part of a growing body of evidence that says that’s just not true. Energy still plays a big role.”

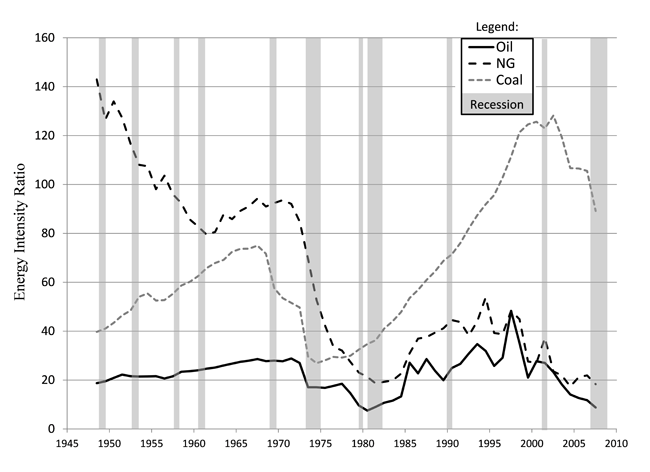

In a paper published this November in the journal Environmental Research Letters, King introduced a new way to measure energy quality, the Energy Intensity Ratio (EIR), that is easier to calculate, highly correlated to EROI and in some ways more powerful than EROI. EIR measures how much profit is obtained by energy consumers relative to energy producers. The higher the EIR, the more economic value consumers (including businesses, governments and people) get from their energy.

When King plots EIR for various fuels every year since World War II, the graphs indicate two large declines, one before the recessions of the mid-1970s and early 1980s and the other during the 2000s, leading up to the current economic recession. There have been other recessions in the U.S. since World War II, but the longest and deepest were preceded by sustained declines in EIR for all fossil fuels.

EIR is proportional to EROI, meaning they rise and fall together, but the basic data behind the EIR calculations come out annually as opposed to every five years for EROI. EIR also gives insight into different parts of the supply chain such as at the refinery or at the gas pump, which are harder to study with EROI.

King’s analysis suggests if EIR falls below a certain threshold, the economy stops growing. For example, in 1972, EIR for gasoline was 5.9 and in 2008 it was 5.5. During times of robust economic growth, such as the 1990s, EIR for gasoline was well over eight. Compare that to some estimates of EROI and EIR for corn ethanol of around one, and it’s clear why corn ethanol has been widely criticized as a low quality energy source.

To get the U.S. economy growing again, King says Americans will have to produce and use energy more efficiently. That’s essentially what the U.S. did after the last energy crisis by raising fuel efficiency standards for cars, increasing use of natural gas for electric power generation and developing new technologies such as Enhanced Oil Recovery to coax more oil out of the ground.

“If we aren’t fundamentally changing the way we produce or consume energy now, don’t expect the economy to grow as much as the past two decades,” he says.

Also See:

Energy intensity ratios as net energy measures of United States energy production and expenditures

For more information about research at the Jackson School, contact J.B. Bird at jbird@jsg.utexas.edu, 512-232-9623.